A non-fungible token (NFT) represents a digital version of real-world objects like art, music, videos, and other NFT utilities like tickets. It's meant to be unique or has high scarcity. It can be bought, traded and sold online with cryptocurrency and fiat currency.

Research shows that in the first half of 2021, NFT sales totalled $2.47 billion.

NFTs have gripped the public's imagination in the last few years. And many are considering investing in NFTs. Before starting with NFTs, you'll need something to store your crypto and the digital assets you acquire in the crypto space.

This is where NFT wallets come in.

You'll need to know have a wallet not only to buy, sell or trade crypto and NFTs, but you'll also need to have them to store and keep safe from NFT scams.

What is an NFT wallet?

An NFT wallet is a digital wallet that stores NFTs and cryptocurrencies in one place. The wallet can receive additional digital assets sent to the wallet holder alongside buying other digital assets.

The considerable increase in NFT purchases in the past few years (see trading volumes above) has led to the further development of NFT wallet functionality for storing the NFT after minting or purchasing. Interestingly, an NFT wallet does not have the assets in a digital version of a particular bank account.

To summarise, an NFT wallet is a physical device or computer program that allows users to store and transfer digital assets like non-fungible tokens and cryptocurrency.

How do NFT wallets work?

Being a technological product, NFT wallets involve a bit of technical NFT vocabulary. However, the way they work is relatively straightforward.

In short, when you create an NFT wallet, it automatically generates a series of words known as a 'seed phrase' (also known as a 'recovery phrase'). The wallet uses the seed phrase to create a set of private keys.

Wallet holders should never share their seed phrase or private keys with anyone, or they will be able to access the assets in the wallet, and the wallet holder will become the victim of NFT fraud.

Understanding how a crypto wallet work is like thinking of it as a password manager for your digital assets. The seed phrase acts as the master password for the wallet – it allows the holder to access their crypto wallet. If the holder deletes their crypto wallet, they can recreate it and access everything using the seed phrase.

However, suppose a holder loses or forgets their seed phrase. In that case, they will lose access to the wallet and all the assets the NFT wallet contains forever. There have been numerous examples of NFT wallet holders forgetting their private keys and thus cannot access millions of dollars worth of cryptocurrency.

Private keys are like passwords.

They allow wallet holders to access and manage the specific items in their wallets. Specifically, the private key lets holders initiate transactions called 'signing.'

Types of NFT wallets

There are three basic types of crypto wallets: software and hardware wallets and a vault.

Hardware wallet, also known as a 'cold wallet'

A hardware wallet is a physical device similar to a USB stick that you might use to store files from your computer. Except that, in this case, you are keeping your crypto and NFTs.

Well-known cold wallets include Ledger and Trezor. To access the data and assets stored on this cold wallet, users will need to physically plug the device into their computer.

The cold wallet will keep digital currencies and NFT assets instead of being stored online within a server. Because hardware wallets are not connected to a server, they are often considered to be in 'cold storage', thus the term cold wallets.

Moreover, even when cold wallets are connected online, the assets stored on the device are almost impossible to steal.

Cold wallet transaction signings are finalised with private keys in-device and then posted to the network via an internet connection. Since private keys never leave the device, malware can't obtain the information needed to falsify a signature.

Software wallet, also known as a 'hot wallet'

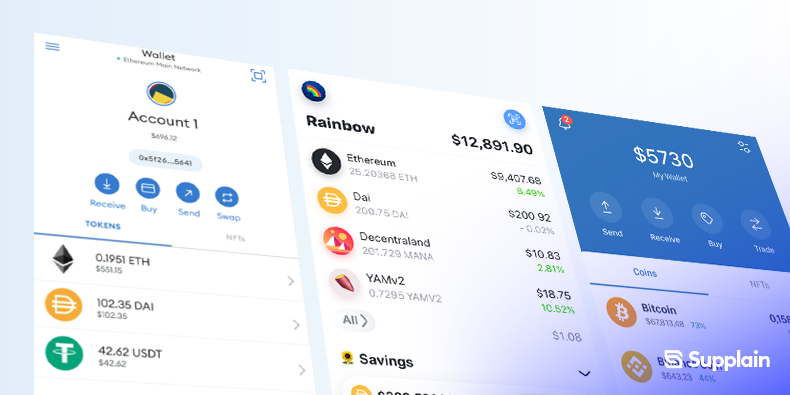

A software wallet is an application or computer program that can be downloaded and installed on a desktop or mobile device. Known software wallets include MetaMask, Rainbow Wallet and Coinbase Wallet. Typically, software wallets are far more convenient and accessed quicker than hardware wallets because the NFT wallets' private keys are stored online.

As the NFT wallet remains connected to the internet, unlike hardware wallets that are considered ‘cold’ - software wallets are considered 'hot.' Many NFT marketplaces require users to use a hot wallet to facilitate transactions, making this type of wallet the primary choice for quick and easy trading.

However, as hot wallets are always connected online and to a server, they are far more likely to open to scams and attacks and thus more likely to be hacked and therefore are considered less secure.

Vaults

Sometimes, crypto users' money is in different places. This is similar to why we keep some cash in a bank account and a savings account. Similarly, cryptocurrency holders can organise funds into different wallets or store their crypto assets in a vault, like Gnosis, one of the most popular vaults.

A vault can receive cryptocurrency and digital assets like a standard NFT wallet. Still, adding optional security steps can also prevent stored assets from being immediately withdrawn.

- Users can invite trusted individuals to co-sign withdrawals, which requires them to approve a transaction before users can complete it.

- Vaults also go through a secure approval withdrawal process after creation. Unapproved vault withdrawals will be cancelled within 24 hours.

Which NFT wallet to choose? Which is best for me?

A hot wallet is a way to go regarding minting and shorter-term trades. However, crypto and NFT holders should use a cold wallet to store their most valuable assets for enhanced security.

MetaMask is a well-known hot wallet used to manage NFT transactions, and it's great for novices looking to set up their first software wallets. MetaMask and others like Coinbase Wallet and Rainbow Wallet connect to a mobile or desktop web browser, allowing users to log in and facilitate transactions on NFT marketplaces and platforms.

If you're interested in hardware wallets, then Ledger and Trezor are two solid brands you can trust. For vaults, our community prefers Gnosis.

We asked our community which do they use, and the consensus was the following:

"Three wallets are best practice, a hot wallet for minting (buying NFTs), a cold wallet for buying and selling on OpeaSea, and a vault that uses signing with keys in separate locations."

Whichever NFT wallet a user decides, it is imperative they must follow the instructions to set up the wallet, physically write down the seed recovery phrase, and store it in a safe place.

What do NFT platforms use?

Presently, we are witnessing a massive revolution in the world of technology - with more of our assets being stored online, known as the metaverse.

Subsequently, the demand to securely access and store our online digital presence and assets means we need an NFT wallet. Therefore, getting the basics, such as an NFT wallet, is vital to have the best in this emerging metaverse.

Several NFT marketplaces, like MakersPlace and Nifty Gateway, allow users to purchase and sell their NFTs using traditional fiat payment methods. Other marketplaces like OpenSea and SuperRare insist users buy, trade and sell NFTs using a cryptocurrency, making a hot wallet needed to use their sites. (Although OpenSea supports fiat payments via a MoonPay integration).

The Ethereum blockchain and its native ETH cryptocurrency is the leading blockchain ecosystem used for facilitating NFT transactions. Trading platforms like Coinbase and Binance allow users to buy cryptocurrencies like Ether with a credit card or bank account debit card, making them more accessible for everyday users.

However, Ethereum isn't the only blockchain network where NFT sales happen. Considering the Ethereum network's high transaction costs and higher environmental impact, crypto-artists and NFT enthusiasts have continued seeking new blockchain ecosystems to create and trade NFTs.

However, if you're still a beginner, it is probably best to stick to Ethereum, as it is seen as the one-stop shop for NFTs and one of the most popular cryptocurrencies and blockchains. Plus, as it's the most trusted and due to its more expensive gas fees, there are fewer scams happening on the network.

![Here are the best NFT games [Updated List]](https://strapi.supplain.io/uploads/What_is_so_special_about_a_World_of_Freight_NFT_and_what_will_move_the_project_forward_b89946b520.png)